Easy [CHE] Easy — Minimalist Pine Script for detecting EMA direction changes to define fixed price zones for simple support and resistance visualization, ideal for manual trading workflows.

Summary

This indicator's programming is kept minimalist and super simple, with core logic in under 20 lines for easy comprehension and modification. It creates fixed price zones based on divergences between a base exponential moving average and its smoother counterpart, helping traders spot potential consolidation or reversal areas without dynamic adjustments. By locking the zone at the high and low of the signal bar, it avoids over-expansion in volatile conditions, offering a stable reference line colored by price position relative to the zone. This approach differs from expanding channels by prioritizing simplicity and persistence until a new qualifying signal, reducing visual clutter while highlighting directional bias through midpoint coloring.

Motivation: Why this design?

Traders often face noisy signals from moving averages that flip frequently in sideways markets or lag during breakouts, leading to premature entries or missed opportunities. This indicator addresses that by focusing on confirmed direction shifts between the base and smoothed averages, then anchoring a non-expanding zone to capture the initial price range of the shift. The result is a cleaner tool for marking equilibrium levels, assuming price respects these bounds in ranging or mildly trending conditions.

What’s different vs. standard approaches?

- Reference baseline: Traditional moving average crossovers or simple channels that update every bar.

- Architecture differences:

- Zones are set only on new divergence signals and remain fixed until reset by a gap from the prior zone.

- No ongoing high-low expansion; relies on persistent variables to hold bounds across bars.

- Midpoint plotting with conditional coloring based on close position, plus a highlight for zone initiations.

- Practical effect: Charts show persistent horizontal references instead of drifting lines, making it easier to gauge if price is rejecting or embracing the zone—useful for avoiding false breaks in low-volatility setups.

How it works (technical)

The indicator first computes a base exponential moving average of closing prices over a user-defined length, then applies a second exponential moving average to smooth that base. It checks if both the base and smoothed values are increasing or decreasing compared to their prior values, indicating aligned direction. A signal triggers when this alignment breaks, marking a potential shift.

On a new signal, if the current bar's high and low fall outside any existing zone (or none exists), the zone bounds update to those extremes and persist via dedicated variables. The midpoint of these bounds becomes the primary plot line, colored green if below the close (bullish lean), red if above (bearish lean), or gray otherwise. A secondary thick line highlights the midpoint briefly when a zone first sets, aiding visual confirmation. No higher timeframe data or external fetches are used, so updates occur on each bar close without lookahead.

Parameter Guide

EMA Length — Sets the period for the base moving average; longer values smooth more, reducing signal frequency but increasing lag. Default: 50. Trade-offs/Tips: Shorter for faster response in intraday charts (risks noise); longer for daily trends (may miss early shifts).

Smoother Length — Defines the period for the secondary smoothing on the base average; higher values dampen minor wiggles for stabler direction checks. Default: 3. Trade-offs/Tips: Keep low (2–5) for sensitivity; increase to 7+ if zones trigger too often in choppy markets, at cost of delayed signals.

Reading & Interpretation

The main circle plot at the zone midpoint serves as a dynamic equilibrium line: green suggests price is above the zone (potential strength), red indicates below (potential weakness), and gray shows containment within bounds (neutral consolidation). A sudden thick foreground line at the midpoint flags a fresh zone start, prompting review of the prior bar's context. Absence of a plot means no active zone, implying reliance on price action alone until the next signal.

Practical Workflows & Combinations

- Trend following: Enter long on green midpoint after a higher low touches the zone lower bound, confirmed by structure like higher highs; filter shorts similarly on red with lower highs.

- Exits/Stops: Use the opposite zone bound as a conservative stop (e.g., below lower for longs); trail aggressively to midpoint on strong moves, tightening near gray neutrality.

- Multi-asset/Multi-TF: Defaults work across forex and stocks on 1H–Daily; for crypto volatility, shorten EMA Length to 20–30. Pair with volume oscillators for confirmation, avoiding isolated use.

Behavior, Constraints & Performance

- Repaint/confirmation: Plots update on bar close using historical closes, so confirmed signals hold; live bars may shift until close but without future references.

- security()/HTF: Not used, eliminating related repaint risks.

- Resources: Minimal overhead—no loops, arrays, or bar limits exceeded; suitable for real-time on any timeframe.

- Known limits: Fixed zones may lag in strong trends (price drifts away without reset); signals skip if no gap from prior zone, potentially missing clustered shifts. Assumes standard OHLC data; untested on non-equity assets.

Sensible Defaults & Quick Tuning

Start with EMA Length at 50 and Smoother Length at 3 for balanced daily charts. If signals fire too frequently (e.g., in ranges), extend EMA Length to 100 for fewer but stabler zones. For sluggish response in trends, drop Smoother Length to 2 and EMA Length to 30, monitoring for added noise. In high-vol setups, widen both to 75/5 to filter extremes, trading speed for reliability.

What this indicator is—and isn’t

This is a lightweight visualization layer for EMA-driven zones, aiding manual chart reading and basic signal spotting. It is not a standalone system, predictive model, or automated alert generator—integrate with broader analysis like market structure and risk rules. (Unknown/Optional: No built-in alerts or multi-timeframe scaling.)

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Cerca negli script per "Heikin Ashi"

VWAP – Pivot Pairs (SECONDS‑BASED RESET)VWAP – Pivot Pairs (SECONDS-BASED RESET) is a Pine Script v6 indicator for TradingView that combines pivot-based breakout detection with resettable VWAP (Volume Weighted Average Price) calculations over user-defined rolling time periods in seconds.It identifies high and low swing pivots via breakout logic, then calculates two VWAP lines per anchor:One using high/low as the price source,

One using close as the price source.

These form "pivot pairs" that reset automatically at the start of each custom-duration period (e.g., every 300 seconds), starting from a user-defined UTC time of day (default: 09:30 UTC).Visuals include:Colored VWAP lines (high pair: red, low pair: green),

Semi-transparent fill zones between each pair,

Optional toggles to show/hide high or low pairs.

Use CasesUse Case

Description

Intraday Scalping (1–15 min charts)

Use 60–300 second resets to capture micro-trends within larger sessions. VWAP pairs act as dynamic support/resistance after breakouts.

High-Frequency / Algo Validation

Backtest strategies on tick/second charts where traditional session resets fail. Align resets with exchange micro-sessions or volatility windows.

Opening Range Breakout (ORB) Enhancement

Set period_seconds = 1800 (30 min) and start time = 09:30 UTC → VWAP builds only on first 30 mins post-open, then floats. Pairs show deviation from ORB mean.

Range-Bound Market Analysis

In choppy markets, VWAP pairs converge near fair value. Divergence signals potential breakout. Fill color intensity shows conviction.

Multi-Timeframe Confluence

Overlay on 1-second chart with 300s reset → matches 5-minute structure. Use close-based VWAP for entries, high/low-based for stops.

Key Features SummaryFeature

Function

period_seconds

Rolling window length in seconds (e.g., 300 = 5 min)

period_start_time

UTC time-of-day anchor (default: 09:30)

new_period logic

Triggers full reset of pivots + VWAP on exact second boundary

breakingHigher / breakingLower

Detects confirmed breakouts (not just close above high)

Dual VWAP per anchor

ta.vwap(high) and ta.vwap(close) for range-aware mean

Fill zones

Visual value area between high/close VWAPs

Toggle visibility

Independently show/hide high or low pivot pairs

How It Works – Step-by-StepTime Engine Converts user inputs → milliseconds

Calculates current period start time using integer division from epoch

Detects exact bar when new period begins (new_period = true)

On New Period Resets both high/low anchors to current bar’s h and l

Forces VWAP recalculation from this bar forward

Breakout Detection Only triggers on strong candles (rising/falling, non-doji)

Requires open/close beyond prior pivot → avoids wicks-only breaks

VWAP Accumulation ta.vwap(source, reset_condition) restarts when anchor resets

Two sources per side → shows where volume clustered (at highs vs closes)

Plotting Four lines + two fills

Clean, customizable, overlay-friendly

Pro TipsUse on Heikin Ashi for smoother breakout signals.

Combine with volume profile to validate VWAP clusters.

For crypto, set period_start_time = 0 (00:00 UTC) for clean 4-hour resets.

Add alerts on new_period or breakingHigher for automation.

In short: This is a precision VWAP tool for time-boxed, pivot-driven mean reversion and breakout trading, ideal for scalpers, day traders, and algo developers needing sub-session granularity.

TopBot [CHE] TopBot — Structure pivots with buffered acceptance and gradient trend visualization

Summary

TopBot detects swing structure from confirmed pivot highs and lows, derives support and resistance levels, and switches trend only after a buffered and accepted break. It renders labels for recent structure points, maintains dynamic support and resistance lines that freeze on contact, and colors candles using a gradient that reflects consecutive trend persistence. The gradient communicates strength without extra panels, while the buffered acceptance reduces fragile flips around key levels. Everything runs in the main chart for immediate context.

Motivation: Why this design?

Classical swing tools often flip on single-bar spikes and produce lines that extend forever without acknowledging when price invalidates them. This script addresses that by requiring a user-controlled buffer and a run of consecutive closes before changing trend, while also freezing lines once price interacts with them. The gradient color layer communicates regime persistence so users can quickly judge whether a move is maturing or just starting.

What’s different vs. standard approaches?

Baseline reference: Simple pivot labeling and unbuffered break-of-structure tools.

Architecture differences:

Buffered level testing using ticks, percent, or ATR.

Acceptance logic that requires multiple consecutive closes.

Synchronized structure labeling with a single Top and Bottom within the active set.

Progressive support and resistance management that freezes lines on first contact.

Gradient candle and wick coloring driven by consecutive trend counts with windowed normalization and gamma control.

Practical effect: Fewer whipsaw flips, clearer status of active levels, and visual feedback about trend persistence without a secondary pane.

How it works (technical)

The script confirms swing points using left and right bar pivots, then forms a current structure window to classify each pivot as higher high, lower high, higher low, or lower low. Recent labels are trimmed to a user cap, and a postprocess step ensures one highest and one lowest label while preserving side information for the others. Support updates on higher low events, resistance on lower high events. Trend flips only after the close has moved beyond the active level by a chosen buffer and this condition holds for a chosen number of consecutive bars. Lines for new levels extend to the right and freeze once price touches them. A running count of consecutive trend bars produces a strength score, which is normalized over a rolling window, shaped by gamma, and mapped to user-defined dark and neon colors for both up and down regimes. Wick coloring uses `plotcandle`; fallback bar coloring uses `barcolor`. No higher-timeframe data is requested. Signals confirm only after the right-bar lookback of the pivot function.

Parameter Guide

Left Bars / Right Bars (default five each): Pivot sensitivity. Larger values confirm later and reduce noise; smaller values respond faster with more noise.

Draw S/R Lines (default true): Enables support and resistance line creation and updates.

Support / Resistance Colors (lime, red): Line colors for each side.

Line Style (Solid, Dashed, Dotted; default Dotted) and Width (default three): Visual style of S/R lines.

Max Labels & Lines (default ten): Cap for objects to control clutter and resource usage.

Change Bar Color (default true), Up/Down colors (blue, black): Fallback bar coloring when gradients or wick coloring are disabled.

Show Neutral Candles (default false): Optional coloring when no trend is active.

Enable Gradient Bar Colors (default true): Turns on gradient body coloring from the strength score.

Enable Wick Coloring (default true): Colors wicks and borders using `plotcandle`.

Collection Period (default one hundred): Rolling window used to scale the strength score. Shorter windows react faster but vary more.

Gamma Bars / Gamma Plots (defaults zero point seven and zero point eight): Shapes perceived contrast of bar and wick gradients. Lower values brighten early; higher values compress until stronger runs appear.

Gradient Transparency / Wick Transparency (default zero): Visual transparency for bodies and wicks.

Up/Down Trend Dark and Neon Colors: Endpoints for gradient mapping in each regime.

Acceptance closes (n) (default two): Number of consecutive closes beyond a level required before trend flips. Larger values reduce false breaks but react later.

Break buffer (None, Ticks, Percent, ATR; default ATR) and Value (default zero point five) and ATR Len (default fourteen): Defines the safety margin beyond the level. ATR mode adapts to volatility; Percent and Ticks are static.

Reading & Interpretation

Labels: “Top” and “Bottom” mark the most extreme points in the active set; “LT” and “HB” indicate side labels for lower top and higher bottom.

Lines: New support or resistance is drawn when structure confirms. A line freezes once price touches it, signaling that the dynamic phase ended.

Trend: Internal state switches to up or down only after buffered acceptance.

Colors: Brighter neon tones indicate stronger and more persistent runs; darker tones suggest early or weakening runs. When gradients are off, fallback bar colors indicate trend sign.

Practical Workflows & Combinations

Trend following: Wait for a buffered and accepted break through the most recent level, then use gradient intensity to stage entries or scale-ins.

Structure-first filtering: Trade only in the direction of the last accepted trend while price remains above support or below resistance.

Exits and stops: Consider exiting on loss of gradient intensity combined with a return through the most recent structure level.

Multi-asset / Multi-timeframe: Works on liquid symbols across common timeframes. Use larger pivot bars and higher acceptance on lower timeframes. No built-in higher-timeframe aggregation is used.

Behavior, Constraints & Performance

Repaint/confirmation: Pivot confirmation waits for the right bar window; trend acceptance is based on closes and can change during a live bar. Final signals stabilize on bar close.

security/HTF: Not used. No cross-timeframe data.

Resources: Arrays and loops are used for labels, lines, and structure search up to a capped historical span. Object counts are clamped by user input and platform limits.

Known limits: Delayed confirmation at sharp turns due to pivot windows; rapid gaps can jump over buffers; gradient scaling depends on the chosen collection period.

Sensible Defaults & Quick Tuning

Start with the defaults: pivot windows at five, ATR buffer with value near one half, acceptance at two, collection period near one hundred, gamma near zero point seven to zero point eight.

Too many flips: increase acceptance, increase buffer value, or increase pivot windows.

Too sluggish: reduce acceptance, reduce buffer value, or reduce pivot windows.

Colors too flat: lower gamma or shorten the collection period.

Visual clutter: reduce the max labels and lines cap or disable wicks.

What this indicator is—and isn’t

This is a visualization and signal layer that encodes swing structure, level state, and regime persistence. It is not a complete trading system, not predictive, and does not manage orders. Use it with broader context such as higher timeframe structure, session behavior, and defined risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Acknowledgment

Thanks to LonesomeTheBlue for the fantastic and inspiring "Higher High Lower Low Strategy" .

Original script:

Credit for the original concept and implementation goes to the author; any adaptations or errors here are mine.

Smart VWAP FVG SystemSmart VWAP FVG System - Professional Multi-Filter Trading Indicator

📊 OVERVIEW

The Smart VWAP FVG System is an advanced multi-layered trading indicator that combines institutional volume analysis, multi-timeframe VWAP trend confirmation, and Fair Value Gap detection to identify high-probability trade entries. This indicator uses a sophisticated filtering mechanism where signals appear only when multiple independent confirmation criteria align simultaneously.

Recommended Timeframe: 5-minute (M5) or higher. The indicator works best on M5, M15, and M30 charts for intraday trading.

🎯 ORIGINALITY & PURPOSE

This indicator is original because it combines three distinct analytical methods into a unified decision-making system:

Market Profile Volume Analysis - Identifies institutional accumulation/distribution zones

Dual VWAP Filtering - Confirms trend direction using two independent VWAP calculations

Fair Value Gap Detection - Validates institutional interest through price inefficiency zones

The key innovation is the directional filter system: the primary Market Profile generates BUY-ONLY or SELL-ONLY states based on higher timeframe value area reversals, which then controls which signals from the main system are displayed. This creates a multi-timeframe confluence that significantly reduces false signals.

Unlike simple indicator mashups, each component serves a specific purpose:

Market Profile → Direction bias (trend filter)

Primary VWAP (Session) → Short-term trend confirmation

Secondary VWAP (Week) → Medium-term trend confirmation

FVG Detection → Institutional activity validation

🔧 HOW IT WORKS

1. Primary Market Profile Filter (Higher Timeframe)

The indicator calculates Market Profile on a higher timeframe (default: 1 hour) to determine the overall market structure:

Value Area High (VAH): Top 70% of volume distribution

Value Area Low (VAL): Bottom 70% of volume distribution

Point of Control (POC): Price level with highest volume

When price reaches VAH and reverses down → SELL-ONLY mode activated

When price reaches VAL and reverses up → BUY-ONLY mode activated

This higher timeframe filter ensures you're trading in the direction of institutional flow.

2. Dual VWAP System

Two independent VWAP calculations provide multi-timeframe trend confirmation:

Primary VWAP (Session-based): Resets daily, tracks intraday momentum

Secondary VWAP (Week-based): Resets weekly, confirms longer-term trend

Filter Logic:

BUY signals require: Price > Primary VWAP AND Price > Secondary VWAP

SELL signals require: Price < Primary VWAP AND Price < Secondary VWAP

This dual confirmation prevents counter-trend trades during ranging conditions.

3. Fair Value Gap (FVG) Detection

FVG zones identify price inefficiencies where institutional orders were executed rapidly:

Bullish FVG: Gap between candle .high and candle .low (upward imbalance)

Bearish FVG: Gap between candle .high and candle .low (downward imbalance)

The indicator monitors recent FVG formation (lookback: 50 bars) and requires:

Bullish FVG present for BUY signals

Bearish FVG present for SELL signals

FVG zones are displayed as colored boxes and automatically marked as "mitigated" when price fills the gap.

4. Main Trading Signal Logic

The secondary Market Profile (default: 1 hour) generates the actual trading signals:

BUY Signal Conditions:

Price reaches Value Area Low

Reversal pattern confirmed (minimum 1 bar)

Price > Primary VWAP

Price > Secondary VWAP (if filter enabled)

Recent Bullish FVG detected (if filter enabled)

Primary MP Filter = BUY-ONLY or NEUTRAL

SELL Signal Conditions:

Price reaches Value Area High

Reversal pattern confirmed (minimum 1 bar)

Price < Primary VWAP

Price < Secondary VWAP (if filter enabled)

Recent Bearish FVG detected (if filter enabled)

Primary MP Filter = SELL-ONLY or NEUTRAL

All conditions must be TRUE simultaneously for a signal to appear.

📈 VISUAL ELEMENTS

On Chart:

🟢 Green Triangle (▲) = BUY Signal

🔴 Red Triangle (▼) = SELL Signal

🟦 Blue horizontal lines = Value Area zones

🟡 Yellow line = Point of Control (POC)

🟩 Green boxes = Bullish FVG zones

🟥 Red boxes = Bearish FVG zones

🔵 Blue line = Primary VWAP (Session)

⚪ White line = Secondary VWAP (Week)

Info Panel (Top Right):

Real-time status display showing:

Filter Direction (BUY ONLY / SELL ONLY / NEUTRAL)

Active timeframes for both MP filters

FVG filter status and count

VWAP positions (ABOVE/BELOW)

Signal enablement status

Alert status

⚙️ KEY SETTINGS

MP/TPO Filter Settings (Primary Indicator)

MP Filter Time Frame: 60 minutes (controls directional bias)

Filter Value Area %: 70% (standard Market Profile calculation)

Filter Alert Distance: 1 bar

Filter Min Bars for Reversal: 1 bar

Filter Alert Zone Margin: 0.01 (1%)

FVG Filter Settings

Use FVG Filter: Enabled (toggle on/off)

FVG Timeframe: 60 minutes (1 hour)

FVG Filter Mode: Both (require bullish FVG for BUY, bearish for SELL)

FVG Lookback Period: 50 bars (how far back to search)

Show FVG Formation Signals: Optional visual markers

Max FVG on Chart: 50 zones

Show Mitigated FVG: Display filled gaps

Market Profile Settings

Higher Time Frame: 60 minutes (for main signals)

Percent for Value Area: 70%

Show POC Line: Enabled

Keep Old MPs: Enabled (maintain historical profiles)

Primary VWAP Filter

Use Primary VWAP Filter: Enabled

Primary VWAP Anchor Period: Session (resets daily)

Primary VWAP Source: HLC3 (typical price)

Secondary VWAP Filter

Use Secondary VWAP Filter: Enabled

Secondary VWAP Anchor Period: Week (resets weekly)

Secondary VWAP Filter Mode: Both

Secondary VWAP Line Color: White

Trading Signals

Show Trading Signals on Chart: Enabled

Show SELL Signals: Enabled

Show BUY Signals: Enabled

Alert Distance: 1 bar

Min Bars for Reversal: 1 bar

Alert Zone Margin: 0.01 (1%)

Retest Search Period: 20 bars

Min Bars Between Retests: 5 bars

Show Only Retests: Disabled

Alert Settings

Enable Trading Notifications: Enabled

VAH Reversal Alert: Enabled (SELL signals)

VAL Reversal Alert: Enabled (BUY signals)

Time Filter Settings

Filter Alerts By Time: Optional (exclude specific hours)

⚠️ IMPORTANT WARNINGS & LIMITATIONS

1. Repainting Behavior

CRITICAL: This indicator uses lookahead=barmerge.lookahead_on to access higher timeframe data immediately for FVG detection. This is necessary to provide real-time FVG zone visualization but has the following implications:

FVG zones may shift slightly until the higher timeframe candle closes

FVG detection signals are preliminary until HTF bar confirmation

The main trading signals (triangles) appear on confirmed bars and do not repaint

Best Practice: Always wait for the current timeframe bar to close before acting on signals. The filter status and FVG zones are informational but may adjust as new data arrives.

2. Minimum Timeframe

Do NOT use on timeframes below 5 minutes (M5)

Recommended: M5, M15, M30 for intraday trading

Higher timeframes (H1, H4) can also be used but will generate fewer signals

3. Multiple Filters Can Block Signals

By design, this indicator is conservative. When all filters are enabled:

Signals appear ONLY when all conditions align

You may see extended periods with no signals

This is intentional to reduce false positives

If you see no signals:

Check the Info Panel to see which filters are failing

Consider adjusting FVG lookback period

Temporarily disable FVG filter to test

Verify VWAP filters match current market trend

4. Market Profile Limitations

Market Profile requires sufficient volume data

Low-volume instruments may produce unreliable profiles

Value Areas update only on higher timeframe bar close

Works best on liquid markets (major forex pairs, indices, crypto)

📖 HOW TO USE

Step 1: Add to Chart

Apply indicator to M5 or higher timeframe chart

Ensure chart shows volume data

Use standard candles (NOT Heikin Ashi, Renko, etc.)

Step 2: Configure Settings

Primary MP Filter TF: Set to 60 (1 hour) minimum, or 240 (4 hour) for swing trading

Main MP TF: Set to 60 (1 hour) for intraday signals

FVG Timeframe: Match or exceed main MP timeframe

Leave other settings at default initially

Step 3: Understand the Info Panel

Monitor the top-right panel:

FILTER STATUS: Shows current directional bias

NEUTRAL = Both signals allowed

BUY ONLY = Only green triangles will appear

SELL ONLY = Only red triangles will appear

FVG Filter: Shows if bullish/bearish gaps detected recently

VWAP positions: Confirms trend alignment

Step 4: Take Signals

For BUY Signal (Green Triangle ▲):

Wait for green triangle to appear

Check Info Panel shows ✓ for BUY signals

Confirm current bar has closed

Enter long position

Stop loss: Below recent VAL or swing low

Target: Previous Value Area High or 1.5-2× risk

For SELL Signal (Red Triangle ▼):

Wait for red triangle to appear

Check Info Panel shows ✓ for SELL signals

Confirm current bar has closed

Enter short position

Stop loss: Above recent VAH or swing high

Target: Previous Value Area Low or 1.5-2× risk

Step 5: Risk Management

Risk per trade: Maximum 1-2% of account equity

Position sizing: Adjust based on stop loss distance

Avoid trading: During major news events or time filter periods

Multiple confirmations: Look for confluence with price action (support/resistance, trendlines)

🎓 UNDERLYING CONCEPTS

Market Profile Theory

Developed by J. Peter Steidlmayer in the 1980s, Market Profile organizes price and volume data to identify:

Value Areas: Where 70% of trading activity occurred

POC: Price level with highest acceptance (most volume)

Imbalances: When price moves away from value quickly

This indicator uses TPO (Time Price Opportunity) calculation method to build the volume profile distribution.

VWAP (Volume Weighted Average Price)

VWAP represents the average price weighted by volume, showing where institutional traders are positioned:

Price above VWAP = Bullish (institutions accumulated lower)

Price below VWAP = Bearish (institutions distributed higher)

Using dual VWAP (Session + Week) creates multi-timeframe trend alignment.

Fair Value Gaps (FVG)

Also known as "imbalance" or "inefficiency," FVG occurs when:

Price moves so rapidly that a gap forms in the candlestick structure

Indicates institutional order flow (large market orders)

Price often returns to "fill" these gaps (rebalance)

The 3-candle FVG pattern (gap between candle and candle ) is widely used in ICT (Inner Circle Trader) methodology and Smart Money Concepts.

🔍 CREDITS & CODE ATTRIBUTION

This indicator builds upon established technical analysis concepts and combines multiple methodologies:

1. Market Profile / TPO Calculation

Concept Origin: J. Peter Steidlmayer (Chicago Board of Trade, 1980s)

Code Inspiration: TradingView's public domain Market Profile examples

Modifications: Custom filtering logic for directional bias, dual timeframe implementation

2. VWAP Calculation

Concept Origin: Standard financial instrument (widely used since 1980s)

Code Base: TradingView built-in ta.vwap() function (public domain)

Modifications: Dual VWAP system with independent anchor periods, custom filtering modes

3. Fair Value Gap Detection

Concept Origin: Inner Circle Trader (ICT) / Smart Money Concepts methodology

Code Implementation: Original implementation based on 3-candle gap pattern

Features: Multi-timeframe detection, automatic mitigation tracking, visual zone display

4. Pine Script Framework

Language: Pine Script v6 (TradingView)

Built-in Functions Used:

ta.vwap() - Volume weighted average price

request.security() - Higher timeframe data access

ta.change() - Period detection

ta.cum() - Cumulative volume

time() - Timestamp functions

Note: All code is original implementation. While concepts are based on established trading methodologies, the combination, filtering logic, and execution are unique to this indicator.

📊 RECOMMENDED INSTRUMENTS

Best Performance:

Major Forex Pairs (EURUSD, GBPUSD, USDJPY)

Stock Indices (ES, NQ, SPX, DAX)

Major Cryptocurrencies (BTCUSD, ETHUSD)

Liquid Stocks (high daily volume)

Avoid:

Low-volume altcoins

Illiquid stocks

Exotic forex pairs with wide spreads

⚡ PERFORMANCE TIPS

Start Conservative: Enable all filters initially

Reduce Filters Gradually: If too few signals, disable Secondary VWAP filter first

Match Timeframes: Keep MP Filter TF and FVG TF at same value

Backtest First: Review historical performance on your preferred instrument/timeframe

Combine with Price Action: Look for support/resistance confluence

Use Time Filter: Avoid low-liquidity hours (optional setting)

🚫 WHAT THIS INDICATOR DOES NOT DO

Does not guarantee profits - No trading system is 100% accurate

Does not predict the future - Based on historical patterns

Does not replace risk management - Always use stop losses

Does not work on all instruments - Requires volume data and liquidity

Does not provide exact entry/exit prices - Signals are zones, not precise levels

Does not account for fundamentals - Purely technical analysis

📜 DISCLAIMER

This indicator is provided for educational and informational purposes only. It is not financial advice, and past performance does not guarantee future results.

Trading Risk Warning:

All trading involves risk of loss

You can lose more than your initial investment (leverage products)

Only trade with capital you can afford to lose

Always use appropriate position sizing and risk management

Consider seeking advice from a licensed financial advisor

Technical Limitations:

Indicator may repaint FVG zones until HTF bar closes

Signals are based on historical patterns that may not repeat

Market conditions change and no system works in all environments

Volume data quality varies by exchange/broker

By using this indicator, you acknowledge these risks and agree that the author bears no responsibility for trading losses.

📞 SUPPORT & UPDATES

Questions? Comment on this publication

Issues? Describe the problem with chart screenshot

Feature Requests? Suggest improvements in comments

Updates: Will be published as new versions using TradingView's update feature

📝 VERSION HISTORY

Version 1.0 (Current)

Initial public release

Multi-filter system: MP + Dual VWAP + FVG

Directional bias filter

Real-time info panel

Comprehensive alert system

Time-based filtering

Thank you for using Smart VWAP FVG System!

Happy Trading! 📈

Fractional + Heikin-Ashi Candlestick – CF / ABNew model of Candlestick, Tis model constructed on Fractional Calculus mathematical, use two kernel - Caputo-Fabrizio and Atangana-Baleanu.

Ben's BTC Macro Fair Value OscillatorBen's BTC Macro Fair Value Oscillator

Overview

The **BTC Macro Fair Value Oscillator** is a non-crypto fair value framework that uses macro asset relationships (equities, dollar, gold) to estimate Bitcoin's "macro-driven fair value" and identify mean-reversion opportunities.

"Is BTC cheap or expensive right now?" on the 4 Hour Timeframe ONLY

### Key Features

✅ **Macro-driven**: Uses QQQ, DXY, XAUUSD instead of on-chain or crypto metrics

✅ **Dynamic weighting**: Assets weighted by rolling correlation strength

✅ **Mean-reversion signals**: Identifies when BTC is cheap/expensive vs macro

✅ **Validated parameters**: Optimized through 5-year backtest (Sharpe 6.7-9.9)

✅ **Visual transparency**: Live correlation panel, fair value bands, statistics

✅ **Non-repainting**: All calculations use confirmed historical data only

### What This Indicator Does

- Builds a **synthetic macro composite** from traditional assets

- Runs a **rolling regression** to predict BTC price from macro

- Calculates **deviation z-score** (how far BTC is from macro fair value)

- Generates **entry signals** when BTC is extremely cheap vs macro (dev < -2)

- Generates **exit signals** when BTC returns to fair value (dev > 0)

### What This Indicator Is NOT

❌ Not a high-frequency trading system (sparse signals by design)

❌ Not optimized for absolute returns (optimized for Sharpe ratio)

❌ Not suitable as standalone trading system (best as overlay/confirmation)

❌ Not predictive of short-term price movements (mean-reversion timeframe: days to weeks)

---

## Core Concept

### The Premise

Bitcoin doesn't trade in a vacuum. It's influenced by:

- **Risk appetite** (equities: QQQ, SPX)

- **Dollar strength** (DXY - inverse to risk assets)

- **Safe haven flows** (Gold: XAUUSD)

When macro conditions are "good for BTC" (risk-on, weak dollar, strong equities), BTC should trade higher. When macro conditions turn against it, BTC should trade lower.

### The Innovation

Instead of looking at BTC in isolation, this indicator:

1. **Measures how strongly** BTC currently correlates with each macro asset

2. **Builds a weighted composite** of those macro returns (the "D" driver)

3. **Regresses BTC price on D** to estimate "macro fair value"

4. **Tracks the deviation** between actual price and fair value

5. **Signals mean reversion** when deviation becomes extreme

### The Edge

The validated edge comes from:

- **Extreme deviations predict future returns** (dev < -2 → +1.67% over 12 bars)

- **Monotonic relationship** (more negative dev → higher forward returns)

- **Works out-of-sample** (test Sharpe +83-87% better than training)

- **Low correlation with buy & hold** (provides diversification value)

---

## Methodology

### Step 1: Macro Composite Driver D(t)

The indicator builds a weighted composite of macro asset returns:

**Process:**

1. Calculate **log returns** for BTC and each macro reference (QQQ, DXY, XAUUSD)

2. Compute **rolling correlation** between BTC and each reference over `corrLen` bars

3. **Weight each asset** by `|correlation|` if above `minCorrAbs` threshold, else 0

4. **Sign-adjust** weights (+1 for positive corr, -1 for negative) to handle inverse relationships

5. **Z-score normalize** each reference's returns over `fvWindow`

6. **Composite D(t)** = weighted sum of sign-adjusted z-scores

**Formula:**

```

For each reference i:

corr_i = correlation(BTC_returns, ref_i_returns, corrLen)

weight_i = |corr_i| if |corr_i| >= minCorrAbs else 0

sign_i = +1 if corr_i >= 0 else -1

z_i = (ref_i_returns - mean) / std

contrib_i = sign_i * z_i * weight_i

D(t) = sum(contrib_i) / sum(weight_i)

```

**Key Insight:** D(t) represents "how good macro conditions are for BTC right now" in a normalized, correlation-weighted way.

---

### Step 2: Fair Value Regression

Uses rolling linear regression to predict BTC price from D(t):

**Model:**

```

BTC_price(t) = α + β * D(t)

```

**Calculation (Pine Script approach):**

```

corr_CD = correlation(BTC_price, D, fvWindow)

sd_price = stdev(BTC_price, fvWindow)

sd_D = stdev(D, fvWindow)

cov = corr_CD * sd_price * sd_D

var_D = variance(D, fvWindow)

β = cov / var_D

α = mean(BTC_price) - β * mean(D)

fair_value(t) = α + β * D(t)

```

**Result:** A time-varying "macro fair value" line that adapts as correlations change.

---

### Step 3: Deviation Oscillator

Measures how far BTC price has deviated from fair value:

**Calculation:**

```

residual(t) = BTC_price(t) - fair_value(t)

residual_std = stdev(residual, normWindow)

deviation(t) = residual(t) / residual_std

```

**Interpretation:**

- `dev = 0` → BTC at fair value

- `dev = -2` → BTC is 2 standard deviations **cheap** vs macro

- `dev = +2` → BTC is 2 standard deviations **rich** vs macro

---

### Step 4: Signal Generation

**Long Entry:** `dev` crosses below `-2.0` (BTC extremely cheap vs macro)

**Long Exit:** `dev` crosses above `0.0` (BTC returns to fair value)

**No shorting** in default config (risk management choice - crypto volatility)

---

## How It Works

### Visual Components

#### 1. Price Chart (Main Panel)

**Fair Value Line (Orange):**

- The estimated "macro-driven fair value" for BTC

- Calculated from rolling regression on macro composite

**Fair Value Bands:**

- **±1σ** (light): 68% confidence zone

- **±2σ** (medium): 95% confidence zone

- **±3σ** (dark, dots): 99.7% confidence zone

**Entry/Exit Markers:**

- **Green "LONG" label** below bar: Entry signal (dev < -2)

- **Red "EXIT" label** above bar: Exit signal (dev > 0)

#### 2. Deviation Oscillator (Separate Pane)

**Line plot:**

- Shows current deviation z-score

- **Green** when dev < -2 (cheap)

- **Red** when dev > +2 (rich)

- **Gray** when neutral

**Histogram:**

- Visual representation of deviation magnitude

- Green bars = negative deviation (cheap)

- Red bars = positive deviation (rich)

**Threshold lines:**

- **Green dashed at -2.0**: Entry threshold

- **Red dashed at 0.0**: Exit threshold

- **Gray solid at 0**: Fair value line

#### 3. Correlation Panel (Top-Right)

Shows live correlation and weighting for each macro asset:

| Asset | Corr | Weight |

|-------|------|--------|

| QQQ | +0.45 | 0.45 |

| DXY | -0.32 | 0.32 |

| XAUUSD | +0.15 | 0.00 |

| Avg \|Corr\| | 0.31 | 0.77 |

**Reading:**

- **Corr**: Current rolling correlation with BTC (-1 to +1)

- **Weight**: How much this asset contributes to fair value (0 = excluded)

- **Avg |Corr|**: Average correlation strength (should be > 0.2 for reliable signals)

**Colors:**

- Green/Red corr = positive/negative correlation

- White weight = asset included, Gray = excluded (below minCorrAbs)

#### 4. Statistics Label (Bottom-Right)

```

━━━ BTC Macro FV ━━━

Dev: -2.34

Price: $103,192

FV: $110,500

Status: CHEAP ⬇

β: 103.52

```

**Fields:**

- **Dev**: Current deviation z-score

- **Price**: Current BTC close price

- **FV**: Current macro fair value estimate

- **Status**: CHEAP (< -2), RICH (> +2), or FAIR

- **β**: Current regression beta (sensitivity to macro)

---

## Installation & Setup

### TradingView Setup

1. Open TradingView and navigate to any **BTC chart** (BTCUSD, BTCUSDT, etc.)

2. Open **Pine Editor** (bottom panel)

3. Click **"+ New"** → **"Blank indicator"**

4. **Delete** all default code

5. **Copy** the entire Pine Script from `GHPT_optimized.pine`

6. **Paste** into the editor

7. Click **"Save"** and name it "BTC Macro Fair Value Oscillator"

8. Click **"Add to Chart"**

### Recommended Chart Settings

**Timeframe:** 4h (validated timeframe)

**Chart Type:** Candlestick or Heikin Ashi

**Overlay:** Yes (indicator plots on price chart + separate pane)

**Alternative Timeframes:**

- Daily: Works but slower signals

- 1h-2h: May work but not validated

- < 1h: Not recommended (too noisy)

### Symbol Requirements

**Primary:** BTC/USD or BTC/USDT on any exchange

**Macro References:** Automatically fetched

- QQQ (Nasdaq 100 ETF)

- DXY (US Dollar Index)

- XAUUSD (Gold spot)

**Data Requirements:**

- At least **90 bars** of history (warmup period)

- Premium TradingView recommended for full historical data

---

## Reading the Indicator

### Identifying Signals

#### Strong Long Signal (High Conviction)

- ✅ Deviation < -2.0 (extreme undervaluation)

- ✅ Avg |Corr| > 0.3 (strong macro relationships)

- ✅ Price touching or below -2σ band

- ✅ "LONG" label appears below bar

**Interpretation:** BTC is extremely cheap relative to macro conditions. Historical data shows +1.67% average return over next 12 bars (48 hours at 4h timeframe).

#### Moderate Long Signal (Lower Conviction)

- ⚠️ Deviation between -1.5 and -2.0

- ⚠️ Avg |Corr| between 0.2-0.3

- ⚠️ Price approaching -2σ band

**Interpretation:** BTC is cheap but not extreme. Consider as confirmation for other signals.

#### Exit Signal

- 🔴 Deviation crosses above 0 (returns to fair value)

- 🔴 "EXIT" label appears above bar

**Interpretation:** Mean reversion complete. Close long positions.

#### Strong Short/Avoid Signal

- 🔴 Deviation > +2.0 (extreme overvaluation)

- 🔴 Avg |Corr| > 0.3

- 🔴 Price touching or above +2σ band

**Interpretation:** BTC is expensive vs macro. Historical data shows -1.79% average return over next 12 bars. Consider exiting longs or reducing exposure.

### Regime Detection

**Strong Regime (Reliable Signals):**

- Avg |Corr| > 0.3

- Multiple assets weighted > 0

- Fair value line tracking price reasonably well

**Weak Regime (Unreliable Signals):**

- Avg |Corr| < 0.2

- Most weights = 0 (grayed out)

- Fair value line diverging wildly from price

- **Action:** Ignore signals until correlations strengthen

Victoria Smart Overlay – EMA1/SMA3/SMA1Core Components:

EMA 1 (Micro): fastest trend trigger

SMA 3 (Short): trend confirmation

SMA 1 (Base): structure guide

Conditions and Actions:

EMA1 crosses above SMA3 → Uptrend starting → Consider Calls / Long

EMA1 crosses below SMA3 → Downtrend starting → Consider Puts / Short

Price hugging SMA1 → Neutral zone → Wait for breakout

Background Green → Confirmed Uptrend → Stay long or scalp Calls

Background Red → Confirmed Downtrend → Stay short or scalp Puts

Micro EMA + Heikin Ashi (Refined Swing Map)

Purpose: Filters fake moves and identifies strong momentum runs.

Use on 5m / 15m charts for intraday clarity.

Signals and Actions:

EMA1 > EMA3 > EMA5 → Micro-uptrend forming → Enter / hold Calls

EMA1 < EMA3 < EMA5 → Micro-downtrend forming → Enter / hold Puts

EMA lines tangled → No conviction → Wait

200-Day SMA rising → Macro bullish → Favor long trades

200-Day SMA falling → Macro bearish → Favor shorts

SevenDayHighLowTableWithBoxes [CHE]SevenDayHighLowTableWithBoxes — Seven-day day-range boxes with a weekday-aware “ghost” projection and a compact table that tracks recent extremes and per-weekday hit rates.

Summary

This indicator visualizes each trading day as a colored box and annotates the final high and low with compact markers. It maintains a rolling seven-day view and a five-column table showing day name, high, low, range, and a per-weekday projection hit statistic. A dashed “ghost” box projects a typical range for the current weekday using a running average and an adjustable scaling factor. The script is written in Pine v6, runs on the main chart (overlay true), and emphasizes stable object handling and closed-bar finalization at day boundaries.

Motivation: Why this design?

Intraday traders often need fast context for where today’s price sits relative to recent daily extremes, without switching timeframes. A simple daily high/low overlay is informative but lacks structure, sizing context, and continuity. By grouping bars into local days (configurable UTC offset), drawing explicit boxes, and projecting a weekday-typical range, the chart becomes easier to scan. The compact table gives a quick audit trail of the latest seven days while tracking how often the weekday projection would have covered the realized range.

What’s different vs. standard approaches?

Reference baseline: Plain daily high/low lines or session boxes without context.

Architecture differences:

Weekday-tinted boxes and labels for today plus up to six prior days.

Weekday average range drives a dashed projection (“ghost”) sized by a user-defined percentage.

Per-weekday hit statistics recorded as hits over totals and displayed in the table.

ATR-based vertical offsets keep labels readable.

Live updates intraday; state is finalized at the local day switch.

Practical effect: The chart shows where current price sits inside a known daily envelope, plus how “typical” the day’s movement is for this weekday, aiding expectations and planning.

How it works (technical)

The script computes a local daily timestamp using the user’s UTC offset. A day change finalizes the prior day, writes its high, low, start and end indices, and records the bar indices of the terminal high and low.

For each weekday, it maintains a running average of realized ranges with a cap on the lookback count. The ghost projection length is the weekday average scaled by the user’s percentage setting.

Anchor selection for the ghost uses the most recent extreme and the close relative to the intraday midpoint to choose a low-anchored or high-anchored box.

A five-column table (Day, High, Low, Range, Ghost OK) is refreshed on the last bar. The “Ghost OK” column shows per-weekday cumulative hits over totals with a percentage, calculated before including the just-finished day.

Object counts are bounded to seven days by pruning arrays and deleting old boxes and labels. Visual updates for historical objects occur on the last bar to minimize overhead. No `security()` calls are used.

Parameter Guide

UTC (+/−) — Controls local day boundaries — Default: minus five hours — Set to your venue’s local time.

Session (for Time gate) — Session string — Default: full week — (Optional) computed internally; not applied to gating.

Show 7-Day High/Low Table — Toggles the table — Default: true — Disable to reduce UI load.

Show Day Boxes in Chart — Toggles day boxes — Default: true — Disable for a cleaner chart.

Table Position — Nine-point anchor — Default: Middle Right — Move to avoid overlap.

Table Background / Text Color / Min Cell Width — Styling controls — Defaults: gray background, white text, width twelve characters.

Weekday Colors (Sun…Sat) — Row and box tints — Defaults: semi-transparent hues — Adjust for your theme.

Triangle Transparency — Marker opacity — Default: zero — Increase to fade high/low dots.

Day Label Transparency — Day name opacity — Default: zero — Increase to reduce emphasis.

Box Border Width — Box stroke width — Default: one — Increase for stronger edges.

Extend Boxes Right — Extend current box — Default: false — Useful for forward planning.

Show Average Range Ghost Box — Dashed projection — Default: true — Disable if distracting.

Ghost Border Color / Width — Ghost styling — Defaults: gray, width one.

Ghost Length percent of AvgRange — Projection scale — Default: one hundred; bounds zero to five hundred — Lower to be conservative.

Max History Days for Average — Cap per-weekday averaging — Default: two hundred fifty-two; bounds thirty to five hundred.

ATR Length / Day Label ATR Multiplier / Triangle Up ATR Multiplier / Triangle Down ATR Multiplier — Offsets for label placement — Defaults: length one hundred; multipliers zero — Increase on dense instruments to prevent overlap.

Reading & Interpretation

Day boxes: The filled rectangle marks each day’s full high-low span; color encodes the weekday.

Markers: Small dots near the terminal high and low highlight where the final extremes occurred.

Ghost box: A dashed box sized by the weekday average range, anchored based on recent behavior. It is a typical span, not a target.

Table: Row one shows “Today”. Rows below list up to six prior days. “Ghost OK” shows per-weekday cumulative hits over totals with a percentage, which reflects historical coverage quality for that weekday.

Practical Workflows & Combinations

Trend following: Use the current box plus recent boxes to read expansion or compression days; combine with basic structure such as higher-highs and higher-lows or lower-lows and lower-highs for confirmation.

Exits and risk: When price nears the ghost boundary late in the session, consider managing exposure more conservatively.

Multi-asset and multi-timeframe: Works on minute charts. As a starting point, use five to less than sixty minutes. For cross-checks, pair with a higher timeframe bias filter.

Behavior, Constraints & Performance

Repaint/confirmation: The indicator updates intraday; extremes and ghost position can move while the day is open. Values are finalized on the next local day start.

HTF/security: None used; repaint risk is limited to live-bar movement.

Resources: `max_bars_back` five thousand; arrays are pruned to seven days; the table and color sync run on the last bar; the live ghost updates only in real time.

Known limits: Weekday averages can be unrepresentative during regime shifts, events, or gaps. Day boundaries depend on the UTC offset being set correctly. No alerts are included. The script displays warning labels when the timeframe is below five minutes or at sixty minutes and above.

Sensible Defaults & Quick Tuning

Start with the defaults.

Ghost too aggressive: Lower the percent scale.

Labels overlap: Increase ATR multipliers.

Clutter or performance issues: Hide the table or boxes, or disable the ghost.

Day boundary misaligned: Adjust the UTC offset to your market.

What this indicator is—and isn’t

This is a visualization and context layer for daily extremes and a weekday-based typical span. It does not predict direction, does not manage orders, and is not a complete trading system. Use it alongside market structure, risk controls, and position management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

MACD Remastered [CHE]MACD Remastered — Robust MACD with confirmed pivot-based divergence, optional signal bands, and ready-to-use alerts.

Summary

This indicator augments classic MACD with a robust, confirmed pivot-based divergence engine and an optional signal channel using Bollinger Bands. Divergence signals are only produced after a pivot is confirmed, which reduces noise from transient swings. A line-of-sight clearance check filters cases where the MACD histogram path contradicts the divergence, further cutting false flags. Histogram coloring clarifies momentum changes, while optional triangles project the same signals onto the main chart for quick context.

Motivation: Why this design?

Standard MACD divergence tools tend to fire early in volatile phases and flip during consolidation. The core idea here is to delay decision points until a pivot is confirmed and to validate the path between pivots. This addresses fake flips and improves signal credibility at the cost of some latency. Optional bands around the Signal line add context about compression and expansion without altering MACD’s core behavior.

What’s different vs. standard approaches?

Reference baseline: Classical MACD (fast and slow moving averages, Signal line, histogram) with simple divergence checks.

Architecture differences:

Confirmed pivot logic with left and right bars.

Line-of-sight clearance test across the histogram path between pivots.

Optional Signal-line Bollinger Bands with configurable length and width.

Composite “Any Divergence” alert plus separate regular and hidden alerts.

Optional main-chart triangles using forced overlay for at-a-glance context.

Practical effect: Fewer early or contradictory divergence signals, clearer momentum context via histogram colors and a visible Signal channel during compression and expansion.

How it works (technical)

The MACD line derives from a fast and a slow moving average on a chosen source. The Signal line smooths the MACD line using a selected moving average type and length. The histogram is the difference between MACD and Signal and is colored by direction and acceleration.

Divergence uses confirmed pivots: a pivot forms only after a set number of bars on the right side, so the event is locked in. The engine retrieves the last two relevant pivots and checks price movement versus the MACD histogram movement to classify regular or hidden divergence. A line-of-sight clearance routine traverses the histogram path between the two pivots and rejects the signal if the path invalidates the directional relationship. When enabled, Bollinger Bands are plotted around the Signal line; width scales with standard deviation. Programmatic alerts fire only on confirmed bars. No higher-timeframe requests are used.

Parameter Guide

Oscillator MA Type — Sets fast and slow MA family for MACD. Default: EMA. Tip: EMA is more responsive; SMA is steadier.

Fast Length — Fast MA period. Default: 12. Trade-off: Shorter is quicker but noisier.

Slow Length — Slow MA period. Default: 26. Trade-off: Longer reduces noise but adds lag.

Source — Price input. Default: Close. Tip: Use a stable source for consistency.

Signal MA Type — Moving average family for Signal. Default: EMA.

Signal Length — Smoothing of MACD into Signal. Default: 9. Trade-off: Longer smooths more, reacts slower.

Calculate Divergence — Enables divergence engine. Default: True.

Enable Bollinger Bands on Signal — Adds bands around Signal. Default: False.

BB Length — Sampling window for bands. Default: 20. Active: Only when bands are enabled.

BB StdDev — Band width in standard deviations. Default: 2.0. Bounds: between about zero point zero zero one and fifty.

Pivot Left / Pivot Right — Bars to the left and right that define a confirmed pivot. Default: five and five. Trade-off: Larger values mean stronger but slower pivots.

Min / Max Bars Between Pivots — Valid window between two pivots. Default: five and sixty. Tip: Increase minimum to reduce micro-divergences.

Detect Hidden — Include hidden divergence. Default: True.

Draw Lines — Draw connector lines on the MACD pane. Default: True.

Alerts: Enable / Regular / Hidden / Frequency / Prefix — Control alert emission, categories, cadence, and label. Defaults: Enabled, both categories on, once per bar close, prefix “MACD RM”.

Reading & Interpretation

Histogram: Columns above zero reflect positive momentum; below zero reflect negative momentum. Color shifts indicate momentum increasing or decreasing within each side.

MACD and Signal: Crosses and distance indicate momentum shifts and strength. When bands are enabled, touches and departures hint at compression and expansion around the Signal.

Divergence: Solid green lines and labels indicate regular bullish; solid red indicate regular bearish. Dashed teal and dashed orange denote hidden bullish and hidden bearish. Triangles on the main chart mirror these events for quicker visibility.

Practical Workflows & Combinations

Trend following: Use histogram color transitions with a structure filter such as higher highs and higher lows for long bias, or lower highs and lower lows for short bias. Divergence against the prevailing structure suggests caution or partial exits.

Exits and risk: In a long, regular bearish divergence near resistance can justify scaling out or tightening stops. Hidden divergence in the trend direction can support continuation but should not replace risk controls.

Multi-asset / Multi-timeframe: Works across liquid futures, forex, indices, and large-cap equities. Start with defaults on four-hour and daily; shorten lengths on intraday only when liquidity is strong.

Behavior, Constraints & Performance

Repaint and confirmation: Signals are anchored only after the right-side pivot bars complete; alerts trigger on confirmed bars. This intentionally adds latency to reduce noise.

No higher-timeframe requests: No `security` calls are used; repaint risk is primarily tied to live bars before confirmation.

Resources: Declared `max_bars_back` is five hundred. The divergence path check iterates between pivots, bounded by the maximum bars parameter. Line objects may accumulate; limits are set for lines and labels.

Known limits: Latency at sharp turns, potential misses during fast single-bar reversals, and sensitivity to extremely choppy sessions if minimum gap between pivots is set too low.

Sensible Defaults & Quick Tunin g

Starting point: EMA, twelve and twenty-six with Signal nine; pivots five and five; minimum five, maximum sixty; alerts on close; bands off.

Too many flips: Increase Signal length, raise pivot counts, and increase minimum bars between pivots. Consider disabling hidden divergence.

Too sluggish: Reduce pivot counts, lower Signal length, and enable bands to visualize early compression.

Cluttered chart: Keep lines off and rely on labels and main-chart triangles. Use the alert prefix to route events cleanly.

What this indicator is—and isn’t

This is a visualization and signal layer for MACD with confirmed, path-checked divergence and optional Signal bands. It is not a trading system, not predictive, and not a position management framework. Use it together with structure analysis, liquidity context, and explicit risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

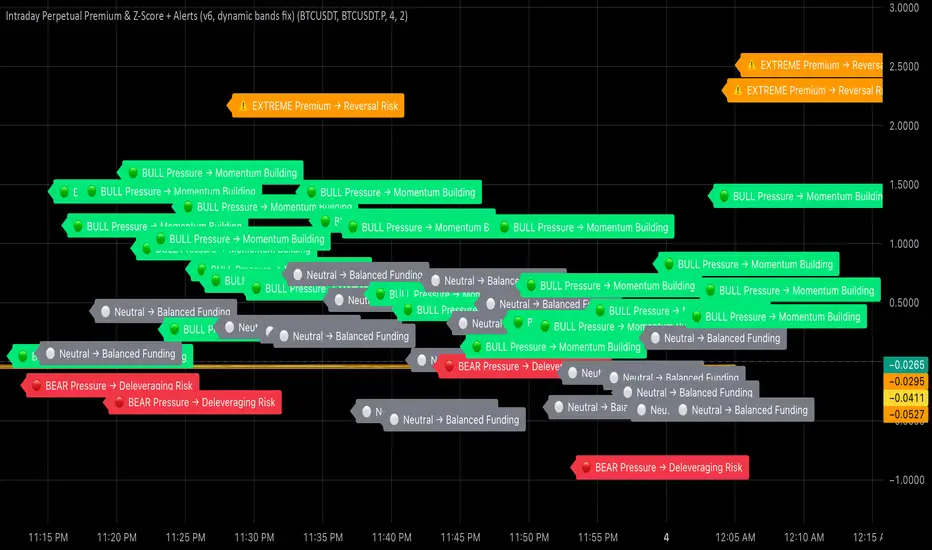

Intraday Perpetual Premium & Z-ScoreThis indicator measures the real-time premium of a perpetual futures contract relative to its spot market and interprets it through a statistical lens.

It helps traders detect when funding pressure is building, when leverage is being unwound, and when crowding in the futures market may precede volatility.

How it works

• Premium (%) = (Perp – Spot) ÷ Spot × 100

The script fetches both spot and perpetual prices and calculates their percentage difference each minute.

• Rolling Mean & Z-Score

Over a 4-hour look-back, it computes the average premium and standard deviation to derive a Z-Score, showing how stretched current sentiment is.

• Dynamic ±2σ Bands highlight statistically extreme premiums or discounts.

• Rate of Change (ROC) over one hour gauges the short-term directional acceleration of funding flows.

Colour & Label Interpretation

Visual cue Meaning Trading Implication

🟢 Green bars + “BULL Pressure” Premium rising faster than mean Leverage inflows → momentum strengthening

🔴 Red bars + “BEAR Pressure” Premium shrinking Leverage unwind → pull-back or consolidation

⚠️ Orange “EXTREME Premium/Discount” Crowded trade → heightened reversal risk

⚪ Grey bars Neutral Balanced conditions

Alerts

• Bull Pressure Alert → funding & premium rising (momentum building)

• Bear Pressure Alert → premium falling (deleveraging)

• Extreme Premium Alert → crowded longs; potential top

• Extreme Discount Alert → capitulation; possible bottom

Use case

Combine this indicator with your Heikin-Ashi, RSI, and MACD confluence rules:

• Enter only when your oscillators are low → curling up and Bull Pressure triggers.

• Trim or exit when Bear Pressure or Extreme Premium appears.

• Watch for Extreme Discount during flushes as an early bottoming clue.

SA_EMA Combo + UT BotEMA Combo + UT Bot is an indicator designed to make it easier to track trend direction and momentum reversals on the same chart.

The indicator combines multiple EMA lines (50/100/150/200) with a short- and medium-term EMA cloud. This cloud visually shows whether the market is in a bullish or bearish trend through color changes.

In addition, it uses the UT Bot algorithm to generate buy and sell signals adapted to market volatility. These signals are triggered when the price crosses the ATR-based trailing stop level.

Users can choose to use Heikin Ashi candles and adjust signal sensitivity via the Key Value parameter. This allows traders to follow overall trends and potential reversal zones using a single tool.

Disclaimer: This indicator is for technical analysis purposes only and should not be considered financial advice.

Developed for Future Alpha Club.

MACD HTF Hardcoded (A/B Presets) + Regimes [CHE] MACD HTF Hardcoded (A/B Presets) + Regimes — Higher-timeframe MACD emulation with acceptance-based regime filter and on-chart diagnostics

Summary

This indicator emulates a higher-timeframe MACD directly on the current chart using two hardcoded preset families and a time-bucket mapping, avoiding cross-timeframe requests. It classifies four MACD regimes and applies an acceptance filter that requires several consecutive bars before a state is considered valid. A small dead-band around zero reduces noise near the axis. An on-chart table reports the active preset, the inferred time bucket, the resolved lengths, and the current regime.

Pine version: v6

Overlay: false

Primary outputs: MACD line, Signal line, Histogram columns, zero line, regime-change alert, info table

Motivation: Why this design?

Cross-timeframe indicators often rely on external timeframe requests, which can introduce repaint paths and added latency. This design provides a deterministic alternative: it maps the current chart’s timeframe to coarse higher-timeframe buckets and uses fixed EMA lengths that approximate those views. The dead-band suppresses flip-flops around zero, and the acceptance counter reduces whipsaw by requiring sustained agreement across bars before acknowledging a regime.

What’s different vs. standard approaches?

Baseline: Classical MACD with user-selected lengths on the same timeframe, or higher-timeframe MACD via cross-timeframe requests.

Architecture differences:

Hardcoded A and B length families with a bucket map derived from the chart timeframe.

No `request.security`; all calculations occur on the current series.

Regime classification from MACD and Histogram sign, gated by an acceptance count and a small zero dead-band.

Diagnostics table for transparency.

Practical effect: The MACD behaves like a slower, higher-timeframe variant without external requests. Regimes switch less often due to the dead-band and acceptance logic, which can improve stability in choppy sessions.

How it works (technical)

The script derives a coarse bucket from the chart timeframe using `timeframe.in_seconds` and maps it to preset-specific EMA lengths. EMAs of the source build MACD and Signal; their difference is the Histogram. Signs of MACD and Histogram define four regimes: strong bull, weak bull, strong bear, and weak bear. A small, user-defined band around zero treats values near the axis as neutral. An acceptance counter checks whether the same regime persisted for a given number of consecutive bars before it is emitted as the filtered regime. A single alert condition fires when the filtered regime changes. The histogram columns change shade based on position relative to zero and whether they are rising or falling. A persistent table object shows preset, bucket tag, resolved lengths, and the filtered regime. No cross-timeframe requests are used, so repaint risk is limited to normal live-bar movement; values stabilize on close.

Parameter Guide

Source — Input series for MACD — Default: Close — Using a smoother source increases stability but adds lag.

Preset — A or B length family — Default: “3,10,16” — Switch to “12,26,9” for the classic family mapped to buckets.

Table Position — Anchor for the info table — Default: Top right — Choose a corner that avoids covering price action.

Table Size — Table text size — Default: Normal — Use small on dense charts, large for presentations.

Dark Mode — Table theme — Default: Enabled — Match your chart background for readability.

Show Table — Toggle diagnostics table — Default: Enabled — Disable for a cleaner pane.

Zero dead-band (epsilon) — Noise gate around zero — Default: Zero — Increase slightly when you see frequent flips near zero.

Acceptance bars (n) — Bars required to confirm a regime — Default: Three — Raise to reduce whipsaw; lower to react faster.

Reading & Interpretation

Histogram columns: Above zero indicates bullish pressure; below zero indicates bearish pressure. Darker shade implies the histogram increased compared with the prior bar; lighter shade implies it decreased.

MACD vs. Signal lines: The spread corresponds to histogram height.

Regimes:

Strong bull: MACD above zero and Histogram above zero.

Weak bull: MACD above zero and Histogram below zero.

Strong bear: MACD below zero and Histogram below zero.

Weak bear: MACD below zero and Histogram above zero.

Table: Inspect active preset, bucket tag, resolved lengths, and the filtered regime number with its description.

Practical Workflows & Combinations

Trend following: Use strong bull to favor long exposure and strong bear to favor short exposure. Use weak states as pullback or transition context. Combine with structure tools such as swing highs and lows or a baseline moving average for confirmation.

Exits and risk: In strong trends, consider exiting partial size on a regime downgrade to a weak state. In choppy sessions, increase the acceptance bars to reduce churn.

Multi-asset / Multi-timeframe: Works on time-based charts across liquid futures, indices, currencies, and large-cap equities. Bucket mapping helps retain a consistent feel when moving from lower to higher timeframes.

Behavior, Constraints & Performance

Repaint/confirmation: No cross-timeframe requests; values can evolve intrabar and settle on close. Alerts follow your TradingView alert timing settings.

Resources: `max_bars_back` is set to five thousand. Very large resolved lengths require sufficient history to seed EMAs; expect a warm-up period on first load or after switching symbols.

Known limits: Dead-band and acceptance can delay recognition at sharp turns. Extremely thin markets or large gaps may still cause brief regime reversals.

Sensible Defaults & Quick Tuning

Start with preset “3,10,16”, dead-band near zero, and acceptance of three bars.

Too many flips near zero: increase the dead-band slightly or raise the acceptance bars.

Too sluggish in clean trends: reduce the acceptance bars by one.

Too sensitive on fast lower timeframes: switch to the “12,26,9” preset family or raise the acceptance bars.

Want less clutter: hide the table and keep the alert.

What this indicator is—and isn’t

This is a visualization and regime layer for MACD using higher-timeframe emulation and stability gates. It is not a complete trading system and does not generate position sizing or risk management. Use it with market structure, execution rules, and protective stops.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Quantum Fluxtrend [CHE] Quantum Fluxtrend — A dynamic Supertrend variant with integrated breakout event tracking and VWAP-guided risk management for clearer trend decisions.

Summary

The Quantum Fluxtrend builds on traditional Supertrend logic by incorporating a midline derived from smoothed high and low values, creating adaptive bands that respond to market range expansion or contraction. This results in fewer erratic signals during volatile periods and smoother tracking in steady trends, while an overlaid event system highlights breakout confirmations, potential traps, or continuations with visual lines, labels, and percentage deltas from the close. Users benefit from real-time VWAP calculations anchored to events, providing dynamic stop-loss suggestions to help manage exits without manual adjustments. Overall, it layers signal robustness with actionable annotations, reducing noise in fast-moving charts.

Motivation: Why this design?

Standard Supertrend indicators often generate excessive flips in choppy conditions or lag behind in low-volatility drifts, leading to whipsaws that erode confidence in trend direction. This design addresses that by centering bands around a midline that reflects recent price spreads, ensuring adjustments are proportional to observed variability. The added event layer captures regime shifts explicitly, turning abstract crossovers into labeled milestones with trailing VWAP for context, which helps traders distinguish genuine momentum from fleeting noise without over-relying on raw price action.

What’s different vs. standard approaches?

- Baseline reference: Diverges from the classic Supertrend, which uses average true range for fixed offsets from a median price.

- Architecture differences:

- Bands form around a central line averaged from smoothed highs and lows, with offsets scaled by half the range between those smooths.

- Regime direction persists until a clear breach of the prior opposite band, preventing premature reversals.

- Event visualization draws persistent lines from flip points, updating labels based on price sustainment relative to the trigger level.

- VWAP resets at each event, accumulating volume-weighted prices forward for a trailing reference.

- Practical effect: Charts show fewer direction changes overall, with color-coded annotations that evolve from initial breakout to continuation or trap status, making it easier to spot sustained moves early. VWAP lines provide a volume-informed anchor that curves with price, offering visual cues for adverse drifts.

How it works (technical)

The process starts by smoothing high and low prices over a user-defined period to form upper and lower references. A midline sits midway between them, and half the spread acts as a base for band offsets, adjusted by a multiplier to widen or narrow sensitivity. On each bar, the close is checked against the previous bar's opposite band: crossing above expands the lower band downward in uptrends, or below contracts the upper band upward in downtrends, creating a ratcheting effect that locks in direction until breached.